Mark Twain once said that a lie can travel halfway around the world while the truth is still pulling on its boots. That was back when social media was what you heard in a tavern. It’s only gotten worse since, and recently, there’s been a freakout over the 15-year car loan. This doesn’t seem to be real, but it’s also not far from reality, which makes the response interesting.

The Morning Dump is wading into affordability, because that seems to be the most pressing issue for the automotive industry. This, and the potential for a 50-year home loan, has created the rumor of a car loan that could stretch to 180 months.

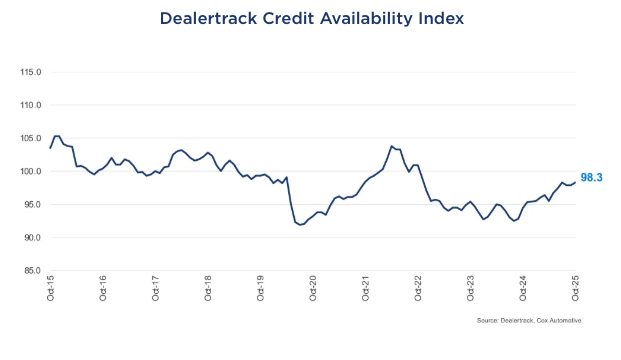

Taking a look at the overall credit market for cars, things are loosening up a little, and car loans themselves are already getting much longer. This isn’t to say all is well in the world of auto financing, as a deep dive into the failure of Tricolor shows how much fraud there potentially is in the system.

As the First Brands (they make all sorts of car parts) bankruptcy demonstrates, getting $10,000 for a car loan might be hard, but getting $100,000,000 for your company on the back of allegedly double-counted invoices is easier than you might guess.

The 15-Year Car Loan Isn’t Real

I woke up this morning and saw that the Autopian Discord (open to everyone) was excited about something. That something had been deleted, but I was able to infer and confirm that it was a rumor about the White House proposing a 15-year car loan. Specifically, there was an image going around in the White House Comms-style saying one was coming, and that Secretaries Lutnick and Duffy were working on it.

This sounded wrong for many reasons, and the post was deleted from Discord after everyone realized it was probably just some social media nonsense. I won’t link to the original because that merely reinforces the problem, but it went viral on both X and BlueSky. There’s a good fact check over on Yahoo! News, and it points out that there’s no version of the fake release on any White House-related accounts.

What tipped me off that it was probably fake was the mention of Secretary of Transportation Sean Duffy. As the old saying goes, the most dangerous place in the world is between Secretary Duffy and a camera, and he hasn’t been out there promoting this.

I think what really made this believable was that President Trump is attempting to address the housing crisis by promoting the 50-year mortgage. The idea there is to potentially lower monthly payments by stretching out the loans. Realtor.com points out one of the reasons why this might not be ideal for homebuyers, and the logic is similar to why it’s not great for people trying to finance a car:

Assuming for the sake of argument that mortgage rates were equal across both products, a 50-year mortgage would lower mortgage payments by about $250 per month on a $400,000 home, assuming 10% down and a 6.25% mortgage rate.

Total interest payments over the life of the 50-year loan would amount to $816,396, compared to $438,156 on the 30-year loan, a difference of $378,240. That amounts to 86% more interest over the life of the loan.

“Buyers do benefit from spreading out the high cost of a home purchase over a longer period, but lenders certainly benefit, too, by having a longer period to charge higher interest rates,” says Berner.

A key difference here is that the main cause of housing costs is a shortage of supply, which this doesn’t address. There’s a way to look at it where the most obvious outcome is that the addition of more buyers without more supply means higher prices. Cars don’t quite have this issue. While there’s some shortage of affordable models, carmakers can more easily turn up production of cars than homebuilders can turn up the supply of affordable housing.

However, homes tend to appreciate in value, whereas cars do exactly the opposite. The bit about interest rates is essentially the same as homes, and that’s worse because cars depreciate so quickly. Doing the math: if someone bought the average car (about $50,000) with the average down payment (about $7,500) at a better-than-average interest rate (7.00%), that person would only have a monthly payment of $382. However, that person would pay $26,261 in interest, making the total payment for the car $76,261 over 15 years. Additionally, the buyer would likely be underwater on the loan for a long period of time.

For all these reasons, a 15-year car loan probably isn’t going to be a White House priority, although there are times when it seems impossible to know these days.

The 15-Year Car Loan Isn’t As Crazy As It Sounds

Car loans are getting longer, with or without White House intervention, and buyers are increasingly underwater. The 84-month loan isn’t that unusual, and, with a slowdown in car buying, lenders are doing more to give access to buyers with lower credit scores.

According to Cox Automotive, the approval rate for auto loans in October hit 72.6%, which is down from September but up from last October. The one area of the market that expanded was subprime lending, with way longer terms being offered to buyers. The latest analysis shows that the share of loans over 72 months is 27.5%, up 300 basis points from last October.

Buyers tend to think in terms of car payments and not the overall market picture, but with rates dropping, these borrowers are not getting the best deal, as Cox points out:

The improvement was driven primarily by lenders’ increased willingness to extend credit to subprime borrowers through longer terms and lower down payments, even as overall approval rates declined. However, this expanded access came with higher yield spreads, meaning consumers paid more for financing compared to prevailing market rates.

Once again, money isn’t everything, but not having it is, especially for subprime borrowers. The longer the loan term, the higher the interest that a lender is going to provide, meaning that as rates go down, borrowers are paying even more for their money.

Tricolor Disaster Shows The Difficulties Facing Subprime Borrowers

The saga of subprime used car retailer Tricolor has revealed a lot about the underwriting practices of large institutional lenders like JPMorgan Chase, but it’s also shown how hard it is to be a subprime borrower.

There’s a great piece from Bloomberg that gets into the chain of events that led to the collapse of Tricolor, which allegedly borrowed money by using the same loans as collateral with multiple lenders. The company’s history is interesting to say the least, but what really got me is how much harder the company was on its borrowers than its lenders seem to have been on Tricolor:

Customers described aggressive sales tactics, confusion over loan documents and long delays in receiving car titles. Some said Tricolor called repeatedly when payments were late, often numerous times a day and deep into the night. Many vehicles were worn out, poorly maintained and had high mileage, according to car buyers and former employees.

Raquel Ramirez says her used GMC Yukon SUV has done nothing but give her trouble since she bought it in 2023 — it constantly jerks when she drives even after repeated repairs — and yet Tricolor staff would hound her when she fell behind on the $35,000 loan she took out. “If I missed a day of a payment, they would call until 10 at night asking for the payment,” Ramirez says.

The lack of scrutiny for massive companies isn’t just an issue with Tricolor. It’s also a key issue in the failure of First Brands.

First Brands Group’s New CEO Admits Company Faked Invoices To Get Loans

First Brands Group, the parent company of brands like Fram and Trico, declared bankruptcy in September after it was discovered that the company had massive debts it wasn’t likely to be able to pay. It was later revealed that the company’s founder, Patrick James, allegedly funneled hundreds of millions of dollars to his own personal accounts.

The company’s new interim CEO, Charles Moore, told the judge handling the bankruptcy that he discovered massive fraud at the company as soon as he arrived.

First Brands lawyers showed a 2022 message from one member of the company’s finance department to another, in which an employee suggests they may have to make “dummy invoices” to secure additional financing. In a subsequent message, a top member of the finance department doesn’t express any concerns about falsifying invoices, Moore testified. That surprised Moore, he said.

“I would think that if the notion of creating a dummy invoice was new or not happening, there would be some reaction to that,” Moore said on the witness stand.

Did you catch that? The new CEO was surprised to find out that the company’s finance department was not surprised to be asked to allegedly commit fraud in order to borrow money.

What I’m Listening To While Writing TMD

Brian kindly took over TMD yesterday, meaning that I missed the opportunity to mark the 50th anniversary of the wreck of the SS Edmund Fitzgerald by playing the eponymous song from Gordon Lightfoot. Today, I fix that.

The Big Question

What car would you take a 180-month loan to buy?

Top photo: Stellantis

The post Why A 15-Year Car Loan Probably Isn’t A Real Thing, Isn’t That Crazy appeared first on The Autopian.